Pandemic-Era Excess Savings Are All Gone

The stash of cash has been slashed

Highlights

• Consumers exhaust pandemic-era excess savings

• Credit card usage slows to a crawl

• Wage inflation concerns are overblown

• Are financial conditions tighter than believed?

While We Were Sleeping

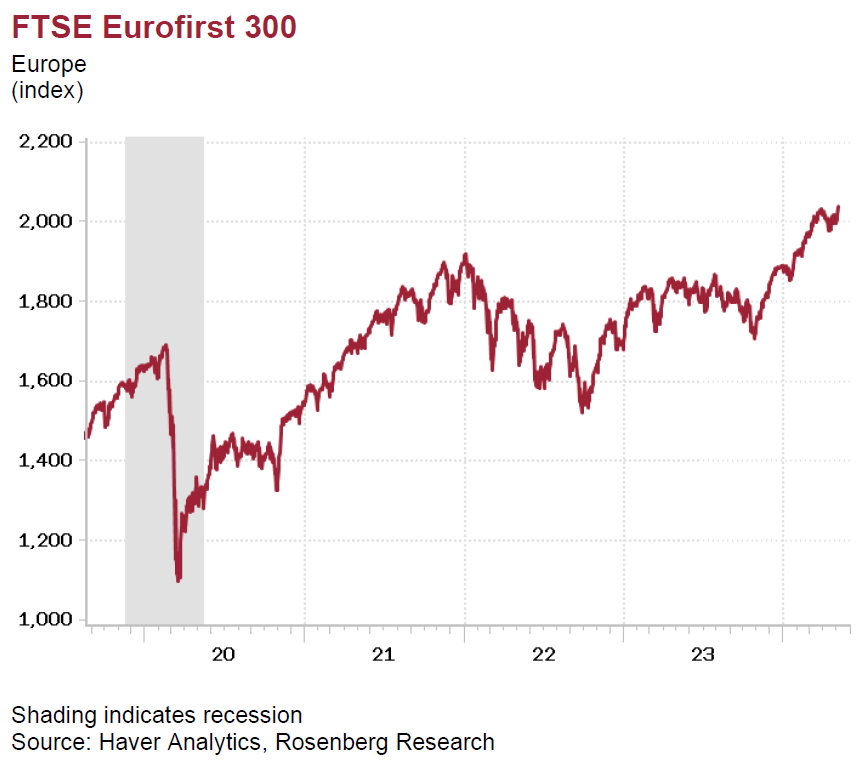

We start the day with U.S. equity futures little changed (swinging from modest gains to modest losses) and Asia facing selling pressure across the board while snapping a four-day winning streak in the process: Japan’s Nikkei 225 (-1.6%), Singapore (-1.2%), Hong Kong (-0.9%), China’s Shanghai Composite (-0.6%), and Thailand (-0.1%). Europe went in the other direction — up +0.5% at the moment and +11.5% YTD for the Euro Stoxx 50 benchmark (versus +8.8% for the S&P 500) as the regional stock market flirts with fresh record highs.

Bond markets are fairly quiet, even with the Riksbank cutting rates -25 basis points at today’s meeting to 3.75% (first easing in eight years) — and hinted that two more such moves are coming by year-end. Sterling is down -0.2% to $1.2485 as easing expectations build from the BoE — it will be interesting to see what the tone is at tomorrow’s policy meeting. The ECB also looks set to follow suit as early as next month, and very likely in the U.K. as well (as BoE Deputy Governor Dave Ramsden, who is considered a trailblazer on the MPC, delivered a speech in April that can only be characterized as dovish).

The DXY dollar index continues to firm alongside the policy divergence between the U.S. and Europe, advancing a further +22 pips to 105.6. Spot gold is little changed, Bitcoin is off -0.9% to $62,377, and Brent crude has given back -0.9% as well to $82.2 per barrel (market quotes are time-stamped to 4:30 a.m. ET).

It was sparse on the data docket, but what we did see was less than stellar, with German industrial production dropping -0.4% MoM in March (though the consensus was at -0.7%), and the YoY trend is mired in negative terrain at -3.3%. This showcases the limitations of just relying on PMI diffusion indices, which look to have been flattering the recovery we are seeing take place across the Atlantic. Meanwhile, preliminary car sales data out of China showed the YoY pace swung to -2% in April from +6% in March.

Must read of the day is the FT editorial on page 14 — The Long Shadows of America’s Growing Debt. This is going to act as a pervasive future constraint on aggregate demand growth, and tackling the largess promises to be a deflationary, not inflationary process.