Historically Low Correlation Between the S&P 500 and GDP

Equity markets are detaching from economic reality

Highlights

• Equity markets are detaching from economic reality

• Odds are skewed to a downside CPI surprise today

• Is the recession already upon us?

• No glow to either of the ISM indices this month

While We Were Sleeping

Well, that was quite the session yesterday, with all the major averages surging more than +1% and on no news whatsoever. It’s all momentum. The price action has been so breathtaking that so far this year, it has outstripped the upward revision to 2025 EPS estimates by a factor of six! Panic buying to kick off the quarter.

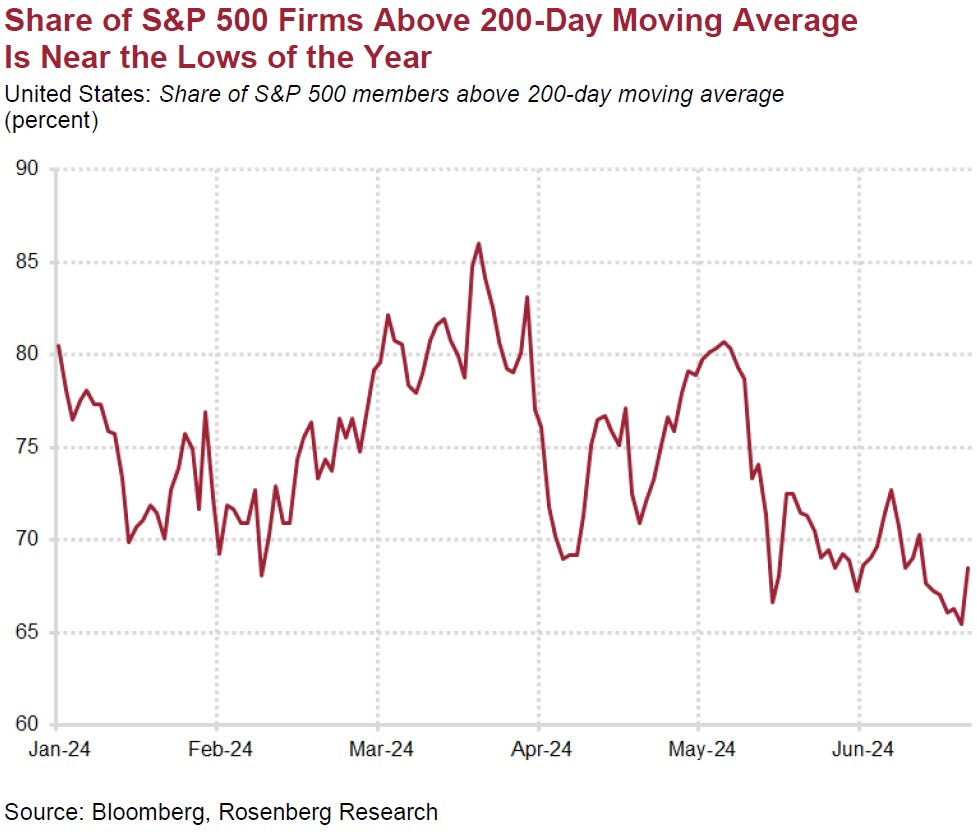

The S&P 500 is riding an epic seven-day winning streak (six record-high closings in a row), the longest in eight months, and breaking above 5,600 for the first time ever. The mega-caps are on fire, with Nvidia jumping +2.7% (up +7.1% so far this week with two days still to go), and the trading volume was incredible with a flurry of 249 million shares — for a $135 stock! Simply amazing. When I started in the business nearly four decades ago, a big trading day would have been 20 million shares. Meanwhile, the share of the S&P 500 trading above the 200-day trendline is stuck near the lows for the year. Only 50% of the index is trading north of the 50-day moving average, a mere 40% for the ripping Nasdaq.

The overnight action is positive, though U.S. futures are down modestly — European markets are up +0.4% at the moment, and Asia enjoyed a very nice session, indeed: Hong Kong (+2.1%), Taiwan (+1.6%), China’s Shanghai Composite (+1.1%), Japan’s Nikkei 225 (+0.9%), Korea (+0.8%), Singapore (+0.5%), India (+0.2%), and Thailand (+0.3%).

In today’s “everything rally,” Bitcoin has perked up +1.2% to $58,316, Brent crude with a +0.6% gain to $85.59 per barrel, and gold inching ahead +0.4% to $2,380 per ounce. Global bond markets are little changed (though perhaps worth noting that Japan’s ultra-long 40-year JGB yield just touched 3% for the first time since this maturity was introduced in 2007); ditto for the forex market, with the DXY dollar index steady at just under the 105 mark (market quotes are time-stamped to 4:30 a.m. ET).

The data calendar was light, but what did come gave an added glow to sterling, already benefitting from relative political stability (especially now that Emmanuel Macron is experiencing intense difficulty in forging a governing coalition in the French parliament) and a stiff-necked BoE that just signaled that rate cuts are not coming that quickly. And now the economic numbers are playing a role, with manufacturing output rocking and rolling +0.4% MoM in May and real GDP matching that advance (+1.4% on a YoY basis which is a veritable boom for virtually any European country). U.K. construction activity also surged +1.9% in May, so something is brewing in the U.K., and it’s not just tea and ale. To little fanfare, sterling has strengthened +4.0% since mid-April against the greenback and by +2.0% versus the euro.

Back to the high-flying U.S. stock market and the story beneath the headline news. Here we have 37 record highs made for the S&P 500 so far this year (27 for the Nasdaq) and yet we now have just 27 stocks at a 52-week high! In the past, the average number of stocks that hit a 52-week high on the same day that the S&P 500 made a new record is 63 and the median is 57. We were less than half those numbers yesterday. Only 0.5% of the time in the past, and we are going back to 1990, have we seen such a dichotomy of so few shares at 52-week highs the same time the index makes a new high. In other words, this is one insane market.

Meanwhile, the VIX, at a lowly 12.85, is a signal that nobody wants to protect against any downside risk. Who needs insurance when you know for a fact that your house will never burn down, or your car won’t get damaged? I shudder to think what happens when this thing breaks — everybody is all in, nobody has rebalanced, taken profits off the table or bothered to purchase downside protection when it is priced at bargain-basement levels.

As for bonds, even with Jay Powell saying he still doesn’t have enough “confidence” that inflation is heading sustainably to the +2% target (“the job is not done on inflation” — going from the +9% peak to barely above +3% clearly isn’t good enough for this dogmatic Fed: when we got there in the mid-1980s under Paul Volcker, everyone was celebrating, but +2% is somehow viewed as a Holy Grail today), the bond market managed to rally modestly on the back of what was another decent Treasury auction.

Add on the fact that Powell sounded concerned just enough about the slack being built up in the labor market that futures are still priced nearly 80% of the way for a September cut. The auction details saw the yield of 4.276% come in one basis point below when-issued pricing; and the bid-to-cover ratio of 2.58 was just above the one-year average of 2.52. Also, direct and indirect bidders took 88.5% of the auction, which is similar to the June auction but the most since last August — kudos to Peter Boockvar for pointing these out.

And we have to say that if the bond market were truly as concerned about fiscal instability as many pundits are, we would be seeing a far greater premium being established at the long end of the Treasury curve. The spread between the 30-year bond yield and the 10-year T-note is a mere +19 basis points. The historical norm is +40 basis points, and we are well below that. We will know that investors are truly getting nervous over the public deficit/debt file when this spread gets to or pierces +100 basis points as was the case in Canada when it confronted its budgetary crisis back in 1994 and the famous 2011 U.S. credit downgrade by S&P.

We keep hearing from many folks that the stock market is nowhere near close to forecasting a recession. But the issue here is that we have the highest concentration in the S&P 500 of stocks that have zero correlation with the business cycle. The longest duration stocks are being valued on expectations of what the total addressable market is going to look like in the AI space over the next five to ten years. The fact that breadth is so horrible and that the average stock has not managed to advance since January 4th, 2022, is a tell-tale sign. The fact that the S&P 500 is now so heavily populated with companies that are not sensitive to the economy means the index itself is becoming increasingly irrelevant as a forecasting tool — over the past 20 and 30 years, the correlation between the S&P 500 and GDP exceeded 50% — today, that correlation has been pared to below 40%.

We sense that today’s CPI number is going to give Powell some added cover as he gingerly moves away from his cautious policy stance. The Manheim index printed negative -0.6% MoM in June, which has implications not just for used cars but also for auto insurance, we know from JD power that there was huge discounting for new vehicles to move excessive inventory off the dealer lots, the rental measures for new leases fell again on a seasonally adjusted basis, and the price war in the fast-food industry was getting into full swing.

The consensus is at +0.2% for the core — I am there too, but see a +0.1% print as more likely than +0.3%, so the distribution curve is skewed for a really good number. Either way, this will mark the best back-to-back readings since July and August of last year. The headline CPI should be weighted down by quite a lot from the price war underway in the fast-food industry, and the same thing for grocery chains. Then tack on the fact that gasoline and fuel prices edged down in June — there should be spillover here to the core index — and we have a nice setup for the 8:30 a.m. (ET) data release.

The chart below is really key in this regard, seeing as one-third of the CPI is represented by rents and OER — the New York Fed’s survey of consumer expectations revealed a huge fall-off in rental rate expectations, to the third lowest pace since December 2020. The -2.6 percentage point plunge in the YoY trend to +6.5% was unprecedented. As of May, the core inflation rate would have been just +1.9% YoY instead of the posted +3.4% pace (from +3.4% a year ago)… now, is that really “sticky?” So, if the New York Fed data manage to get reflected in today’s CPI release, we could well see a very nice downside shocker.

We are currently working on a report as to how Donald Trump’s policies would influence real GDP growth and inflation if he gets elected and manages to carry out his platform. As was the case from November 2016 to November 2020, there was a myriad of moving pieces and several acted to offset the effects of others between restricted immigration, tax cuts, tariffs, and waves of deregulation.

The reality is after everything got thrown into the mix, what we saw was that even with the tariffs, ex-energy import prices and the core goods CPI barely increased at all over that four-year period. Even with the curbs on immigration and the commensurate tightening in the labor market, unit labor costs only managed to expand at a +2.3% annual rate. That is because one critical offset was the impact the broad deregulation moves exerted on productivity, which impressively rose at a +2.7% average annual rate.

And the corporate tax cuts, instead of igniting inflation, did the exact opposite because the nonfarm business price deflator rang in at just a +1.4% annual rate over that four-year period — because the tax relief helped companies fatten their margins without having to resort to any meaningful price increases. By 2019, even Jay Powell figured this out as he embarked on three rate cuts before the pandemic reared its ugly head.

As for the widespread view that Trump’s policies were too protectionist and would result in a shrinkage in trade flows, the reality is that exports and imports combined rose +6% over this piece (though the trade deficit did continue to expand — by nearly +50% — and the view that the tax cuts paid for themselves in Arthur Laffer fashion is laughable because even before COVID-19 arrived, the fiscal deficit under President Trump surged more than 60% from the time the cuts were made and to the time the pandemic-recession kicked us in the gut).